Medicare Advantage Plans: How They Work and What to Expect

When people first start learning about Medicare Advantage plans, one of the biggest questions that comes up is whether they should choose this option or stick with Original Medicare. It’s a fair question, and a lot of people don’t get a clear answer right away. Medicare covers a lot, but the way coverage is delivered can look very different depending on the path you choose. If you don’t understand how these plans actually work and what to expect, you’re not alone. Once you see how they’re structured, it becomes much easier to decide if they might fit your situation.

When people first start learning about Medicare Advantage plans, one of the biggest questions that comes up is whether they should choose this option or stick with Original Medicare. It’s a fair question, and a lot of people don’t get a clear answer right away. Medicare covers a lot, but the way coverage is delivered can look very different depending on the path you choose. If you don’t understand how these plans actually work and what to expect, you’re not alone. Once you see how they’re structured, it becomes much easier to decide if they might fit your situation.

What Medicare Advantage Plans Actually Are

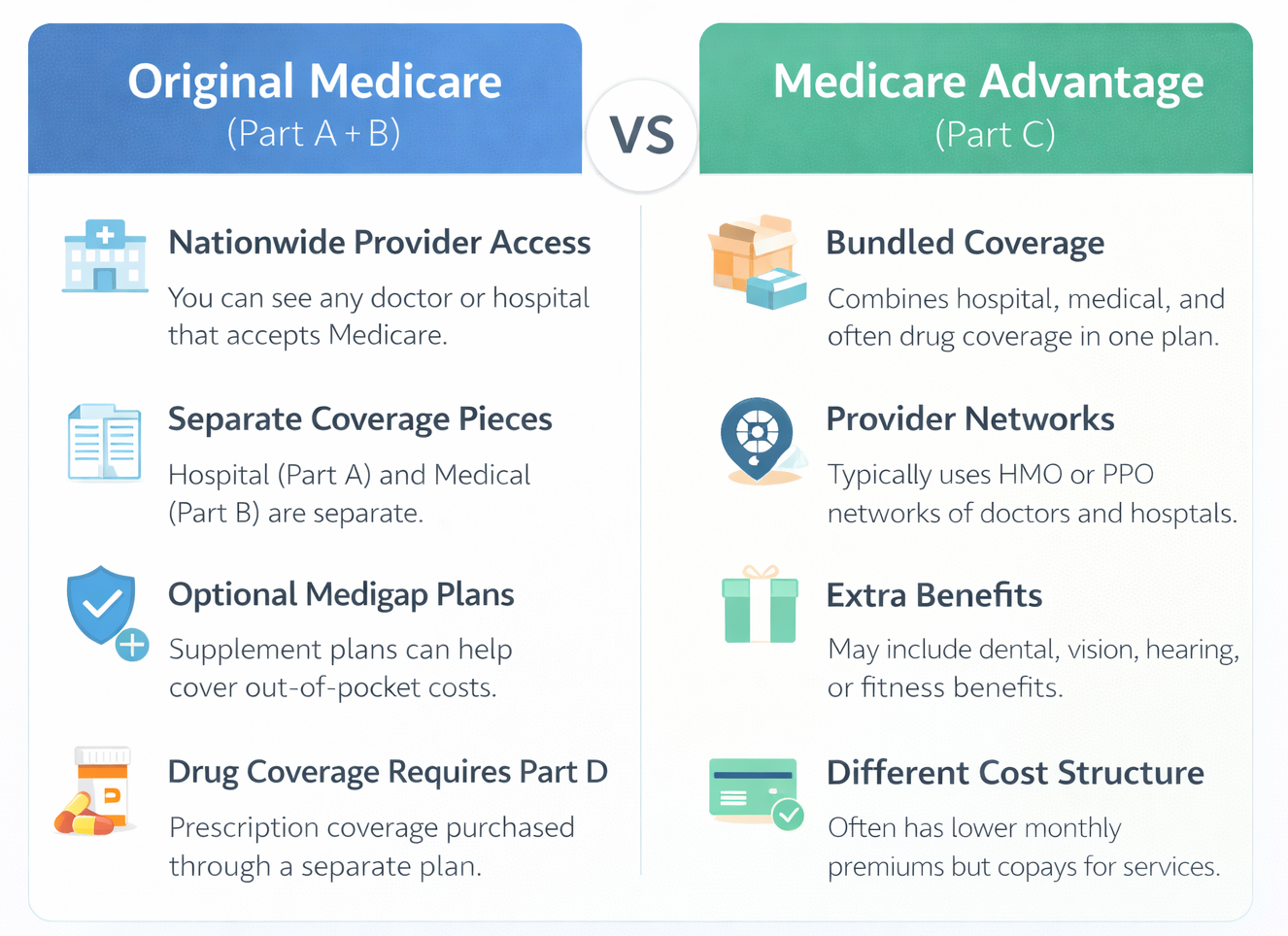

Medicare Advantage plans, also known as Part C, are offered by private insurance companies approved by Medicare. Instead of receiving your benefits directly through Original Medicare, you receive them through one of these plans. The plan still follows Medicare rules, but it manages how your care is delivered. These plans must cover everything that Medicare Part A and Part B cover. However, the way care is structured can feel different from Original Medicare.

How Medicare Advantage Plans Work Day to Day

How Medicare Advantage Plans Work Day to Day

Most of these plans use provider networks such as HMOs or PPOs. That means you’ll typically use doctors and hospitals within the plan’s network to receive the lowest costs. Some plans allow you to go outside the network, but costs may be higher. This structure helps coordinate care, but it also limits flexibility compared to Original Medicare.

What Coverage May Include

What Coverage May Include

Many of these plans include additional benefits beyond standard Medicare coverage. Depending on the plan, this may include prescription drug coverage, dental services, vision care, hearing benefits, fitness programs, etc. This bundled approach makes things feel simpler because multiple types of coverage are combined into one plan. However, benefits vary by plan and location, so it’s important to review the details carefully.

Medicare Advantage Plans Costs and Out-of-Pocket Limits

Medicare Advantage Plans Costs and Out-of-Pocket Limits

Costs work differently compared to other Medicare options. Some plans offer lower monthly premiums, but you may pay more when you receive care through copays or coinsurance. One important feature is the annual maximum out-of-pocket limit. This helps protect you from very high healthcare costs during the year. Because of this structure, it’s important to look at both monthly costs and potential usage when comparing plans.

Why Some People Choose Medicare Advantage Plans

Why Some People Choose Medicare Advantage Plans

Many people choose Medicare Advantage plans because they like having everything bundled together. Instead of managing multiple plans, they can have medical coverage, drug coverage, and additional benefits in one place. Some individuals also prefer lower monthly premiums and are comfortable paying for services as they go. For those who value simplicity, this approach can make sense.

Why This Option May Not Fit Everyone

Why This Option May Not Fit Everyone

At the same time, this type of coverage is not the right fit for everyone. Provider networks can be a limiting factor. If you want to see doctors nationwide without restrictions, this setup may feel restrictive. Costs can also vary depending on how often you use care. While premiums may be lower, out-of-pocket costs can add up over time. That’s why it’s important to think about how you actually use healthcare, not just what the plan looks like upfront.

Medicare Advantage Plans vs Original Medicare

When comparing Medicare Advantage plans to Original Medicare, the biggest difference is how coverage is delivered. Original Medicare allows you to see any provider nationwide who accepts Medicare. Medicare Advantage Plans typically use networks and manage care through a private company. Neither option is automatically better. They simply work differently.

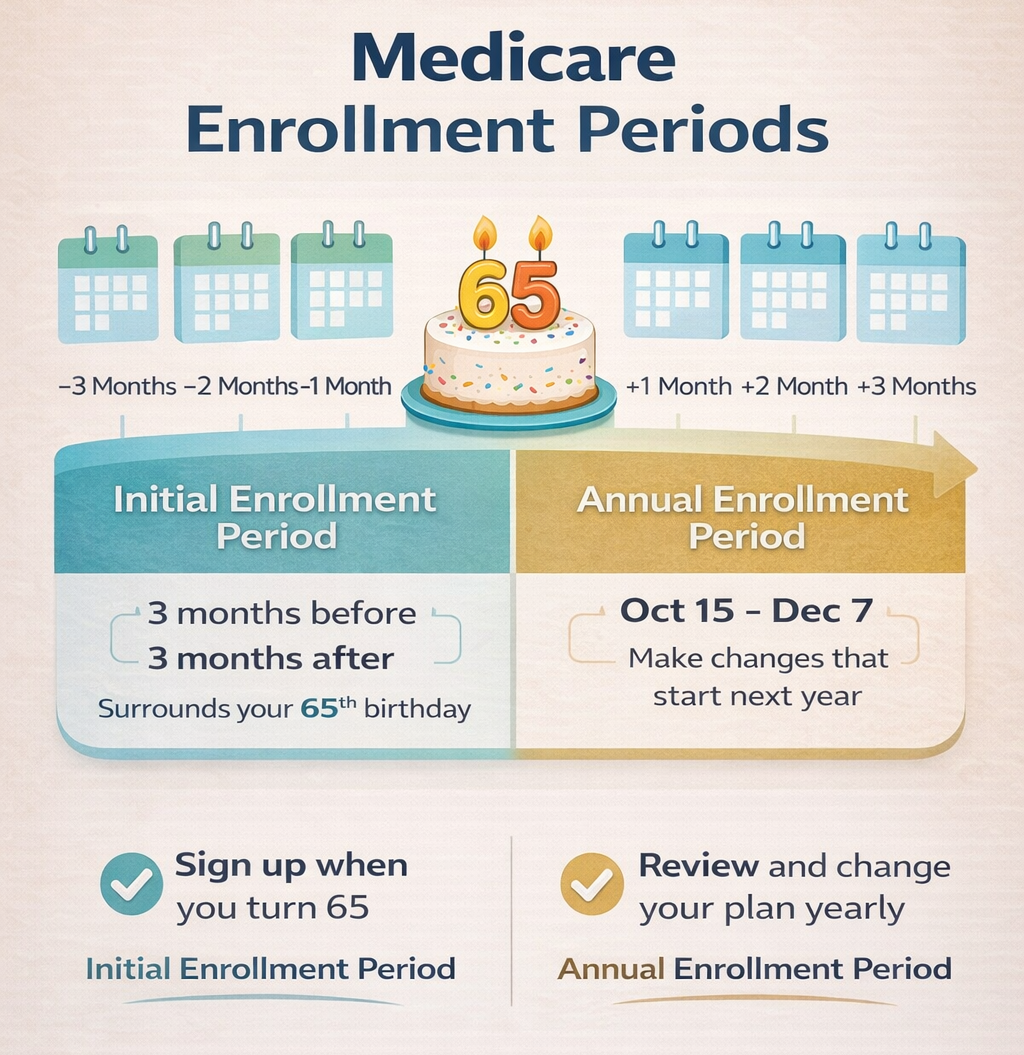

When You Can Enroll in Medicare Advantage Plans

When You Can Enroll in Medicare Advantage Plans

Most people first enroll during their Initial Enrollment Period when they become eligible for Medicare. There is also an Annual Enrollment Period from October 15 through December 7 each year. During this time, you can join, switch, or leave a plan.

Why Reviewing Your Plan Each Year Matters

Even if your plan works well now, things can change. Insurance companies may update costs, provider networks, or covered medications. Taking time to review your options each year helps make sure your coverage still fits your needs.

Talking Through Your Options Can Help

Talking Through Your Options Can Help

At some point, most people want to talk through their options with someone who understands how plans work locally. Not to be pressured, but to get clear answers. A local Medicare broker can explain how plans work in your area, compare options, and help you understand what to expect in a simple way. That conversation alone often makes the decision much easier.

Final Thoughts

These plans can be a good fit for people who prefer bundled coverage and are comfortable using provider networks. For others, a different approach may make more sense. The most important step is understanding how the plan works before making a decision. Do not feel pressured to make a decisions immediately. Once you have that clarity, everything becomes much easier.

Get 1-on-1 AssistanceClick Here

Learn More About Medicare

You may also find these Medicare guides helpful:

Follow us on:

![]()

![]()

![]()

![]()

IMPORTANT NOTE: This information is for educational purposes only and is not a complete description of benefits. Benefits, premiums, and plan availability may vary by location and plan provider. For more information, visit Medicare.gov or speak with a licensed insurance professionals.